By Brenda Carrico

A Long-Term Cost Comparison for Aging Clients

They had lived in the same home for over forty years. It was the house where they raised their kids, celebrated holidays, and built a lifetime of memories. Over time, though, maintenance slowly slipped. Projects were postponed. Updates felt expensive and exhausting.

Whenever the idea of moving came up, the same hesitation surfaced. “We can’t move until we fix the house.” The thought of living through a remodel felt overwhelming. So staying put became the easier choice, even as the home no longer fit their needs.

Eventually, after honest conversations, they chose a different approach.

They sold the home as is, accepted a slightly lower price, and avoided months of disruption and decision fatigue. What they did not anticipate was the all in cost of transitioning to a retirement community and how quickly those expenses added up.

This scenario, for illustrative purposes, is common among aging clients. The decision between staying in your home and moving to a Continuing Care Retirement Community, or CCRC, is rarely just about preference. It is about timing, predictability, care needs, and long-term financial planning.

Which option is more cost effective over the long term?

We hear this question from clients and their family members and although simple on the surface, it’s complex underneath.

The answer depends on your health, lifestyle preferences, and financial priorities.

Using current Kansas and Midwest cost data, we can outline realistic ranges to help frame the discussion.*

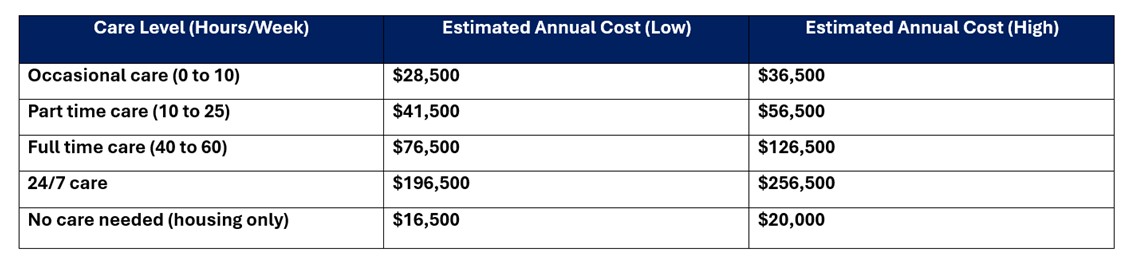

Estimated Annual Cost Comparison: Home vs. CCRC

Staying in Your Home

The cost of remaining in your home varies widely depending on the level of care required over time. Many people assume staying home will always be less expensive, but that is not always the case as care needs increase. Estimated annual costs include property taxes, insurance, utilities, maintenance, and in home care where applicable.

While home costs may feel manageable early on, they are often unpredictable and tend to rise quickly as needs change.

Continuing Care Retirement Community (CCRC)

Most CCRCs in the Kansas and Midwest region provide housing, meals, activities, and access to increasing levels of care as needed. Typical costs include:

This cost range generally applies whether you remain independent or later require assisted living or skilled care, since many CCRCs bundle care into their fee structure. While the upfront transition can feel expensive, the tradeoff can be greater predictability.

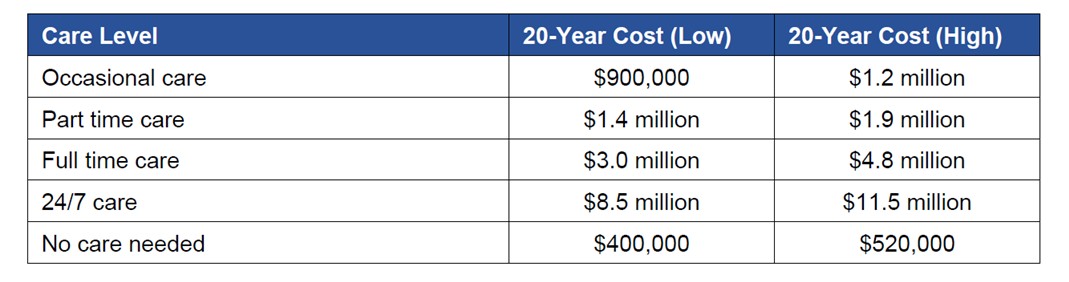

Long Term Cost Projections

The following projections use 5.5 percent healthcare inflation for care services and 3 percent general inflation for housing and CCRC fees.

20 Year Cost Outlook

Staying in Your Home

CCRC

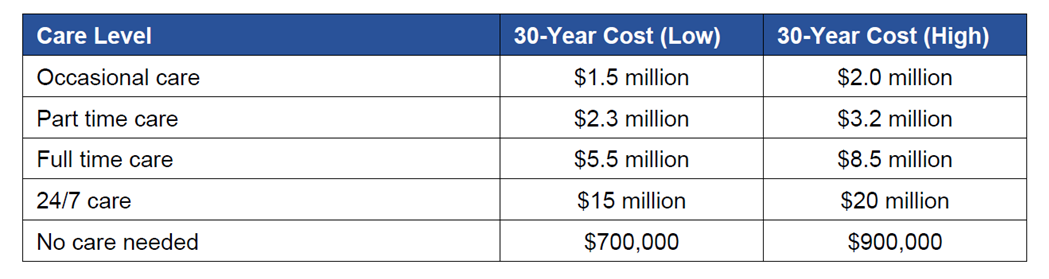

30 Year Cost Outlook

Staying in Your Home

CCRC

What These Numbers Really Mean

If you never need care, staying in your home is significantly less expensive. Over 20 to 30 years, the difference can be hundreds of thousands or even millions of dollars.

If you need part time care, the costs begin to converge, and the decision becomes more about lifestyle, support, and stress.

If you need full time or 24/7 care, staying at home often becomes dramatically more expensive. This is where many families feel caught off guard, especially when care needs escalate faster than expected.

The takeaway is not that one option is always better. It is that CCRCs provide cost stability and built in access to care, while home based care carries increasing financial uncertainty over time.

Why This Matters for Financial Planning

Choosing between aging in place and moving to a retirement community is not just a housing decision. It is a long term financial and lifestyle strategy that deserves thoughtful planning.

At Searcy Financial® Services, we understand there is no single right answer. Some clients want to remain in their homes as long as possible. Others value the predictability and support of a retirement community. Our role is to help you evaluate your options so you can choose the path that best aligns with your preferences, family dynamics, and budget. Understanding these potential cost trajectories helps you.

- Plan for future cash flow needs

- Evaluate whether long term care insurance may be appropriate

- Stress test your portfolio against higher care scenarios

- Make informed decisions about housing, downsizing, and estate planning

We are also happy to serve as a resource for clients aging in whatever direction makes the most sense for them. Navigating later life transitions can feel overwhelming and having a trusted team to help think through the financial and logistical considerations can make those decisions feel more manageable.

If you would like to explore this topic further, the following blog posts written by our team may be helpful.

- Caring Transitions: Helping Families Navigate Life’s Big Moves

- Senior Care Consulting: Expert Guidance for Your Loved Ones

- Professional Guidance and Services to Help Your Loved Ones Age with Dignity

Planning early often provides more flexibility and peace of mind than waiting until change becomes unavoidable.

How Long-Term Care Insurance Can Change the Cost Picture

Long term care insurance can meaningfully impact these projections, but only when the details are fully understood. Policies vary widely in benefit amounts, inflation protection, benefit periods, and the types of care covered. In some cases, a strong policy can narrow the cost gap between staying at home and moving to a CCRC. In other cases, particularly with older or lower benefit policies, the impact may be more limited. Any long-term financial plan should incorporate the specifics of your coverage to understand how it may reduce out of pocket costs over time.

*Important Disclosure

The cost estimates in this article are generalized projections based on publicly available data for the Kansas and Midwest region. Actual costs vary significantly depending on the specific community, level of care, geographic location, inflation, and personal circumstances. This information is intended for educational and planning purposes only and should not be interpreted as personalized financial advice. Clients should consult with their financial planner to evaluate their individual situation.

Sources Available Upon Request