What is the purpose of estate management?

Estate management is about preserving the assets you’ve spent a lifetime building. It’s about protecting your spouse, children, or other heirs and ensuring that your assets are distributed how and when you want them to be. Estate management is also about managing the taxes that may be due after your death.

There are two objectives in effective estate management:

- Managing your financial and personal affairs during your lifetime.; and

- Distributing your wealth after your death.

If properly executed, estate management can make a significant difference by enabling you to spell out your healthcare wishes in ways that may help ensure they are carried out—even if you are unable to communicate. And it can help ensure that your possessions go to the heirs you choose, without the endless legal wrangling that can tie up your estate and cause deep divisions within your family.

Estate planning is an important piece of your overall financial plan.

Through effective estate management, you can help avoid needless legal costs and provide for loved ones who may not be protected otherwise. These issues are too important to trust to luck—you need to determine the outcome by planning in advance.

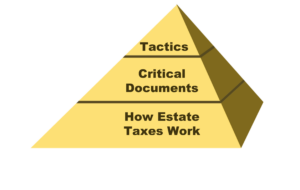

It may be helpful to visualize the various estate management principles and strategies as a pyramid. The foundation is formed by an understanding of how estate taxes work. As we move up, we encounter critical estate management documents and, at the top, specific tactics for estate management.

How Estate Taxes Work

In order to understand how estate taxes work, let’s look at the history of the estate tax. The first estate tax was established in 1797 to fund an undeclared naval war with France. Shortly after the war ended, the tax was revoked.

That happened again for the Civil and Spanish-American wars. Congress passed an estate tax to pay for the war, and then repealed it afterward.

The 16th Amendment to the Constitution was passed in 1913—the one giving Congress the right to “lay and collect taxes on incomes, from whatever source derived.” The Revenue Act of 1916 established an estate tax, which has been modified over the years but never repealed.

In 2012, the American Tax Relief Act made the estate tax a permanent part of the tax code.

In 2017, the Tax Cuts and Jobs Act doubled the estate tax exemption.

In 2024, the estate tax exemption rose to $13.61 million. That law is currently set to expire on December 31, 2025.1

Estimating Your Estate Taxes – “Quick” Formula Example

This hypothetical example shows that the formula for estimating estate taxes is quite simple.

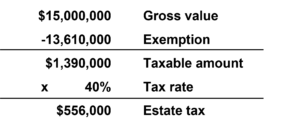

If you don’t happen to have a complete set of IRS tax tables lying about, you can estimate the federal estate tax using a quick formula. Beginning with the gross value of an estate, subtract $13,610,000, the 2024 exemption, from $15,000,000. Then, multiply the result by 40%—the federal tax bracket for estates above $13,610,000. This leaves you with a total of $556,000 in a taxable estate. Keep in mind that the estate tax exemption amount is indexed for inflation and may be adjusted annually. The current estate tax legislation is set to expire on December 31, 2025. 1

If you complete your estimation—and find you may have an estate tax bill—you may benefit from estate management.

Important Documents for Your Estate Plan

A will is the most basic estate planning document. It tells the world exactly where you want your assets distributed when you die.

Everyone should have a will, but according to one study, roughly 68% of American adults don’t have one. 2

Not having a will could be a big headache—and not just for the wealthy—because if an individual dies intestate, or without a will, it’s up to the state to decide how his or her assets will be distributed. Even if you have a trust, you still need a will to take care of any holdings outside of that trust when you die.

A will really is the cornerstone of your estate. Your will names an executor to oversee the process of distributing your estate. It can name a guardian for your minor children. And it can direct how your property is to be distributed.

Unfortunately, as important as they are, wills have shortcomings. Wills can be contested. In fact, the probate court will send out notice of the will to anyone who might have grounds to contest it. And if someone wants to contest it, there is the potential for a lengthy battle in probate court. Since wills are essentially instructions to the probate court, they will likely pass through probate depending on the state. The probate process can be expensive, and it can take many months (or years) to resolve. And probate is a matter of public record. If the only estate management tool you use is a will, anyone who wants to can find out how much you left and to whom.

A will isn’t the only document you need to have in place to take care of your estate. There is a whole set of documents that can help you pursue your estate management goals.

Among these are:

- “Advanced directives,” which include a living will, power of attorney, and the durable power of attorney for healthcare

- Financial documents and agreements, such as joint ownership, durable power of attorney, and living trusts

A living will provides specific instructions about your medical care if you become incapacitated and unable to communicate. It goes into effect immediately upon your incapacity.

A power of attorney document authorizes someone to handle legal and financial decisions when you become incapacitated. It can also go into effect upon your incapacity, or upon any other trigger event you specify. Like a living will, a power of attorney does not need to go through any additional legal proceedings. Individual states have various power of attorney laws. So, consider becoming familiar with your state’s particular regulations to make a more informed decision.

A durable power of attorney for healthcare authorizes someone to make decisions for healthcare on your behalf. And, like the living will and the power of attorney, it does not need to go through any additional legal proceedings.

Would your family know your wishes if you became incapacitated?

Contemporary research shows that about 70% of older Americans complete advance directives before their death.3

With extended life expectancy and various treatment options available, the chance that you or someone close to you will benefit from an advance directive is greater than ever.

Important Financial Documents in Effective Estate Management

Joint ownership is actually a way of holding title to property. It’s useful because if a partner dies, the other can assume ownership without the property having to go through probate. It goes into effect as soon as joint ownership is recorded, and it does not need to go through any additional legal proceedings.

A durable power of attorney allows you to appoint a person or organization to take care of your financial affairs when you cannot do so. It is “durable” because it includes specific language that allows it to remain in effect or to take effect if you become mentally incompetent. It can go into effect immediately or when a specific trigger event occurs—such as your incapacity. Powers of attorney can be rescinded at any time and do not need to go through any additional legal proceedings.

A living trust is a trust created while you are still alive. Living trusts go into effect when the trust documents are signed and the trust is funded—that is, when you’ve transferred assets into it.

Of course, estate management isn’t all documents. There are some basic tactics to understand as well.

The first of these is simple: give money away while you’re still alive.

The tax code allows an individual to gift up to $18,000 per person in 2024 without triggering any gift or estate taxes. If you and your spouse both make gifts, that’s up to $36,000 in 2024. However, if a person gives $19,000 to someone, the person must report the gift on their taxes and deduct $1,000 from his or her lifetime exemption. The annual exclusion amount is indexed for inflation, which is measured by the Consumer Price Index. It rises in $1,000 increments as the CPI increases.

In 2024, an individual can give away up to $13,610,000 during his or her lifetime without owing any federal tax. Couples can leave up to twice that without owing any federal tax. Also, remember that some states may have their own estate tax regulations.4

Trusts are another powerful estate management tool.

A trust is a legal entity that can own property. Properly structured trusts completely avoid probate and avoid the delays and expenses that often accompany probate. Trusts are not a matter of public record. They’re a tool for maintaining privacy.

Trusts can offer effective management of your assets and their distribution to your heirs. And, even after death, trusts can provide some measure of control over how assets are distributed to children and other beneficiaries. Trusts are also much more difficult to contest than a will. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

What should you consider when putting together a management plan for your estate?

There are two crucial factors to consider:

First, what’s the value of your estate? As you make this calculation, make sure you include all the property that you control or have an interest in. This includes personal property, your home, real estate, cash and bank accounts, investments, retirement plans, business interests, and life insurance—including death benefits. In 2024, the gross value of your estate must exceed $13,610,000 for you to be subject to the federal estate tax.1 But even if you are not, you should consider getting your estate and healthcare documents so that your wishes may be carried out.

Second, what are your estate management objectives? Ask yourself the following questions:

- Who do you want to inherit your assets?

- Who do you want handling your financial affairs if you’re ever incapacitated?

- Who do you want making medical decisions for you if you cannot make them for yourself?

- Do you want to provide for your spouse if you die first?

- Do you have young children to provide for?

- If your children are grown, do you want to distribute your estate equitably—if not perfectly equally?

- Will you need to provide cash to help your heirs settle your estate?

Life insurance can also play a critical role in your estate management—particularly when used in conjunction with a trust. Life insurance can provide money to pay for estate expenses. It can be set up outside your estate. You can even gift life insurance policies.

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder may also pay surrender charges and have income tax implications. You should consider whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments. Life insurance is not insured by any federal government agency, bank, or savings association.

Understanding the principles of estate management is important, as is making sure you include estate planning in your overall financial plan and have your documents up to date. If you are in need of a referral to an estate planning team that can meet your needs, we would be happy to make an introduction.

Sources:

- https://www.irs.gov/businesses/small-businesses-self-employed/estate-tax

- https://www.plannedgiving.com/legacy-box/wills-and-estate-planning-statistics/#:~:text=Will%2C%20or%20Will%20Not%3F,made%20plans%20for%20their%20legacy.

- https://pmc.ncbi.nlm.nih.gov/articles/PMC6345507/#:~:text=Like%20other%20means%20of%20prevention,%2C%20&%20Wetle%2C%202007).

- https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes